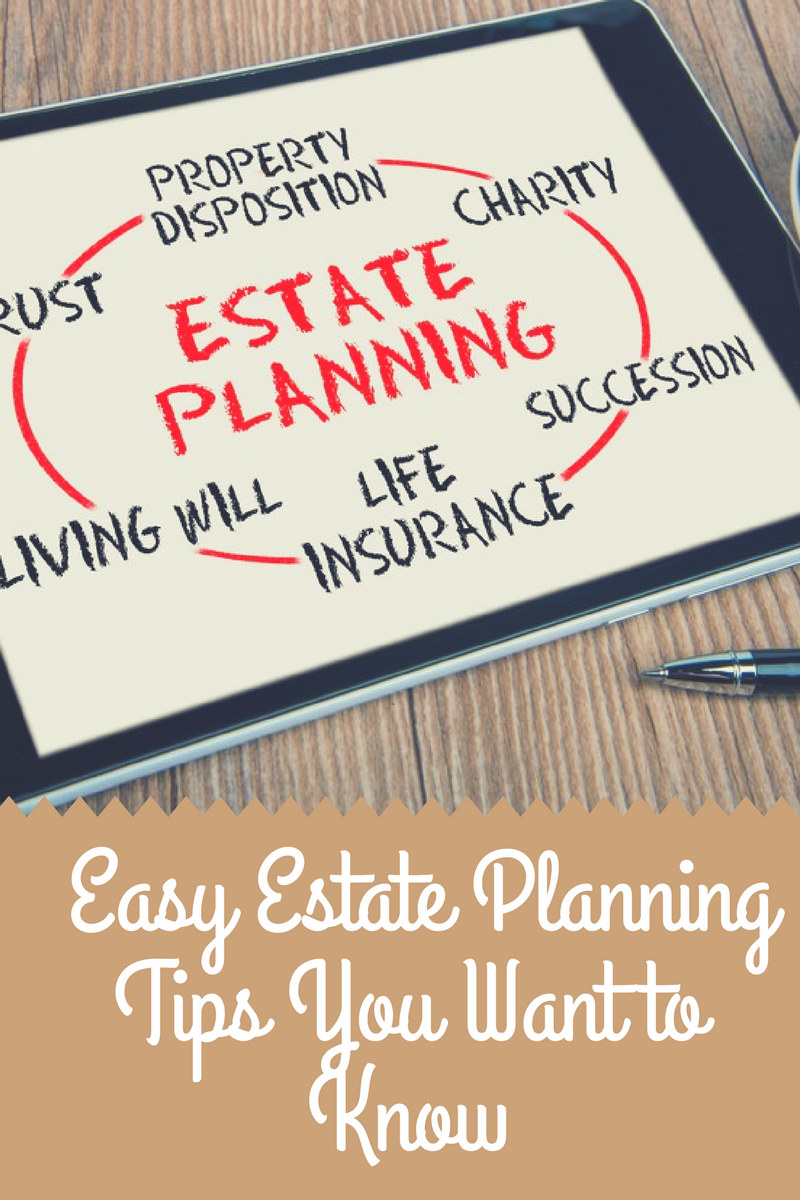

When it comes to financial stability, many people think that means having enough income to get by every month. Additionally, they include paying bills, having a well-established savings account, and having extra for family activities. However, an important step is to secure your children’s future when you pass away. As sad as it sounds, it’s time to plan for the future. Knowing that you have assets and finances is an important aspect for your family’s well being. Their financial stability will be impacted for years to come. So, today we’re sharing parenting tips on estate planning.

One of the things you can do to secure your family’s future financially is to plan an estate. Estate planning isn’t something only rich people should do. It’s a concept that is very much open to anyone who has assets to be distributed. Given the potentially-complex nature of estates, it’s understandable that some people might be overwhelmed. However, knowing what to consider when estate planning may make life easier for you.

According to Forbes, those who file estate plans don’t need to live inside actual estates. Estate planning is simply a legal way to make sure the planner’s family is protected. Additionally, it ensures that the estate is secure upon your death or you become incapacitated. Here are a few estate planning tips you should know:

Can You Leave the Estate to Your Spouse?

One of the ways you can plan your estate is to just transfer everything to your spouse upon your death or if you become incapacitated. This is useful if everything that will be involved in the estate plan is jointly owned between you and your spouse.

You can transfer everything to your spouse as long as the estate tax exemption limit isn’t met by your assets. Should you exceed this, you’ll most likely benefit from two revocable trusts to help reduce the taxes owed to the estate. These trusts can be divided between you and your spouse.

How Do I Ensure My Kids Are Secure and Protected?

Certain states only transfer your assets to your children officially when they reach a particular age. However, it’s impractical to give everything to a 21-year-old in the form of a lump sum. However, you are allowed to name someone who can be responsible for managing the assets and the funds you’ve left to your children. Once they mature, the money can be turned over to them.

- Furthermore, this person doesn’t necessarily have to be a relative or someone close to your children. It has to be someone you trust and someone who will follow your wishes.

Can I Create an Estate Plan After My Child’s Birth?

If you plan on creating an estate plan right after your child is born, you may want to hold off. Make sure you fully understand the estate laws in your state. Furthermore, try to review your documents every three to five years to ensure that everything is in place. Especially, the designation of assets that will be distributed.

You have to be extra careful when naming your children as beneficiaries. For example, if a child develops special needs, it might be helpful if their trust has some form of supplemental needs attached.

What If You Don’t Undergo Estate Planning?

One of our biggest estate planning tips is this one: if you don’t plan your estate, then you may end up in probate court. Most financial professionals try to avoid probate court because it expensive. Additionally, it’s time consuming.

- In probate, the court will decide who receives what. So, the court will assess potential creditors and heirs. From there they will divide your payments and assets to them.

- You can avoid the probate process in a number of ways. One is to create something called a revocable trust. A revocable trust allows you to give ownership of properties and assets to something known as a “trust.” It lists exactly what you want to happen if you pass away or become incapacitated.

- Another way to avoid probate is to start assigning beneficiaries to your assets. These include a tax-deferred account or a life insurance policy. In the event of your passing, your beneficiary will be the one receiving your assets. So, check with a lawyer about these assets, your bank account, home and other assets on hand.

Estate Planning Can Work for Your Benefit

Hopefully, the above estate planning tips will give you a better understanding of estate planning. Once you determine the assets and finances you want to secure, getting help with estate planning can be a good experience. A lawyer or a legal professional can give you a more in-depth understanding of estate planning or litigation. Click here for more information.

About the author: Kiren Manning

About the author: Kiren Manning

Kiren is an estate law writer who enjoys writing about real estate and law. He has written for a few blogs in the past, and enjoys sharing his knowledge with those who enjoy reading. In his spare time he enjoys spending quality time with those he loves.

I’m glad you talked about how a legal professional can help your understanding of estate planning become deeper. It seems like younger people don’t think about estate planning as often because they feel like they still have their whole lives in front of them and don’t need to plan for anything. I feel like it would be important to at least have a full understanding of why estate planning is important even if you don’t need it at this exact moment.

There are many people who simply don’t understand estate planning and how it applies to them. I agree estate planning is important, now it’s a matter of figuring out how to get the information to people. Thanks for stopping by.